Dubai is entering a high-stakes delivery window. Analysts estimate the residential pipeline will deliver between 200,000 and 300,000 new apartments and villas by 2028. Research cited from consultancies such as Knight Frank and independent observers places the figure closer to 260,000 to 303,000 units. The concentration of handovers is projected to peak in 2026 and 2027. That peak matters for pricing, leasing, and absorption, because much of the wave comes from off-plan projects launched during the post-pandemic boom.

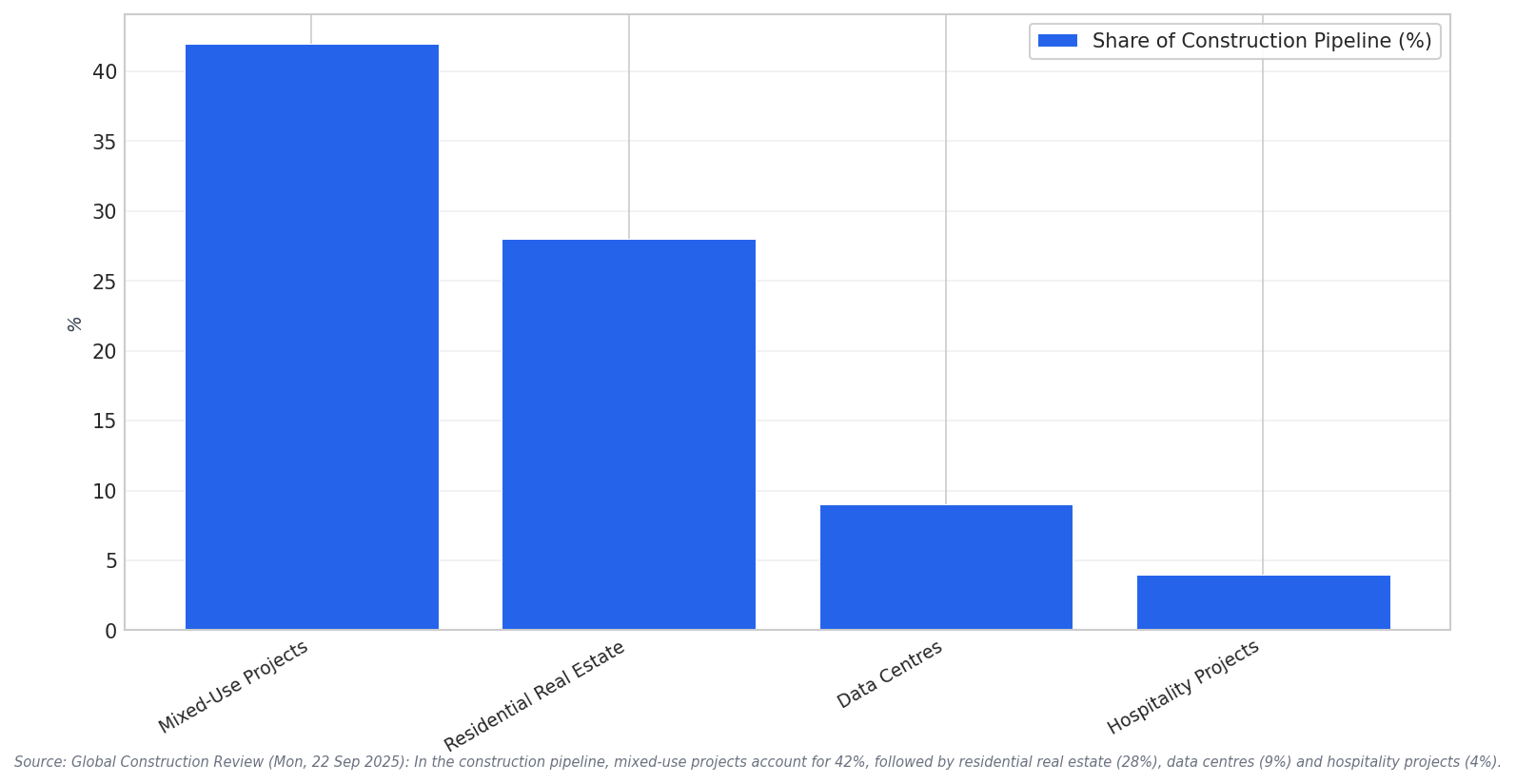

That is where Dubai mixed-use mega projects become the new geometry of urban investment. In the construction pipeline, mixed-use projects account for 42%, ahead of residential real estate at 28%, data centres at 9%, and hospitality projects at 4%. This mix signals that the next growth phase is not only about selling units. It is about combining living, working, and services in one investable district. For investors, that can shift due diligence toward phasing, tenant quality, and how one component supports the others when supply lands at scale.

Why 2026-2027 Changes the Investment Playbook

Experts already frame 2026 and 2027 as the crucial phase for market adjustment. Some analysts foresee moderate corrections, while others point to strong rental demand, immigration, and economic growth as potential cushions. The practical implication is simple. Investors may need to be more selective. A heavy delivery schedule can create localized pressure even when the broader story remains resilient. Mixed-use districts can be evaluated as systems, not single assets, especially when handovers cluster and competition rises between new communities.

Construction activity also shows how capital is being deployed. Construction accounts for 62% of future pipeline projects, ahead of transport at 12%, power at 7%, and water at 5%. In Dubai specifically, project activity is concentrated in the construction sector at 75%. This concentration aligns with the prominence of mixed-use schemes in the pipeline. It also suggests that investors tracking Dubai mixed-use mega projects should monitor construction delivery risk and sequencing, because the market is absorbing a large build cycle across multiple categories at once.

Major named developments underline the breadth of the pipeline. Upcoming projects in Dubai include Palm Jebel Ali, The Oasis by Emaar, Marsa Al Arab, Therme Dubai, Naia Island, Venice at DAMAC Lagoons, plus Parkwood and Address Residences in Dubai Hills Estate. Infrastructure plans sit alongside real estate. Dubai is expanding its Metro system by 15km by 2029 with the construction of the Blue Line. Dubai is also investing over $35 billion to transition from DXB to Dubai World Central by 2032. Together, these moves shape accessibility, demand patterns, and long-run district competitiveness.

What does the keyword “Dubai mixed-use mega projects” refer to in this pipeline context?

How many new residential units are expected in Dubai by 2028?

Why are 2026 and 2027 important for Dubai real estate investors?

What is the sector split of future pipeline projects in the UAE sources?

Which transport projects in the sources could influence district demand?