Saudi Arabia’s Vision 2030 was introduced to diversify the economy beyond oil, with “giga-projects” backed by the Public Investment Fund (PIF) at the center of the strategy. But multiple reports now point to a reset in how these developments are sequenced and financed. CoStar reported a slowdown as Saudi Arabia reassesses diversification plans amid fluctuating oil prices and increased costs, with some projects being reevaluated or extended. Reuters also described delays and recalibrations, citing economic headwinds and logistical constraints. For market participants, this is less about a stop and more about a reprioritization of what moves first.

The progress narrative and the recalibration narrative are both visible at once. Reuters quoted investment minister Khalid Al-Falih saying 85% of Vision 2030 targets were “complete or on track” as of the end of 2024, while also noting that the multi-billion dollar program faces delays and recalibrations. Reuters added that 675 companies now have regional headquarters in Riyadh, reflecting policy traction even as project delivery is adjusted. Investors should read this as a shift toward outcomes that can be measured in operating activity, not only in headline project announcements.

NEOM sits at the center of the Saudi Vision 2030 recalibration story. CoStar said NEOM is undergoing revisions to its blueprint due to escalating costs and economic considerations, with Edward James of MEED saying contract phases will resume after reassessments. Reuters reported NEOM has faced repeated implementation delays and that sources said it has been scaled back as Riyadh prioritizes infrastructure deemed essential for hosting global sporting events such as the 2034 World Cup. Skift also reported that PIF approved its 2026-2030 strategy on April 15, shifting from “rapid growth and acceleration” to “sustained value creation,” and that construction commitments were cut by tens of billions.

What the New Priority Stack Signals to the Market

AGBI reported that a new investment protocol puts Expo 2030 and the 2034 World Cup at the top of the priority list, and quoted a source saying, “No contract of significance is going to be awarded this year unless it’s got the words Expo or World Cup.” The same report said this prioritization extends beyond venues into transportation, mobility and energy infrastructure, and entertainment. For contractors, that implies near-term pipelines tied to event-linked infrastructure packages. For investors, it suggests a clearer demand driver and a more defined schedule anchor than purely speculative developments.

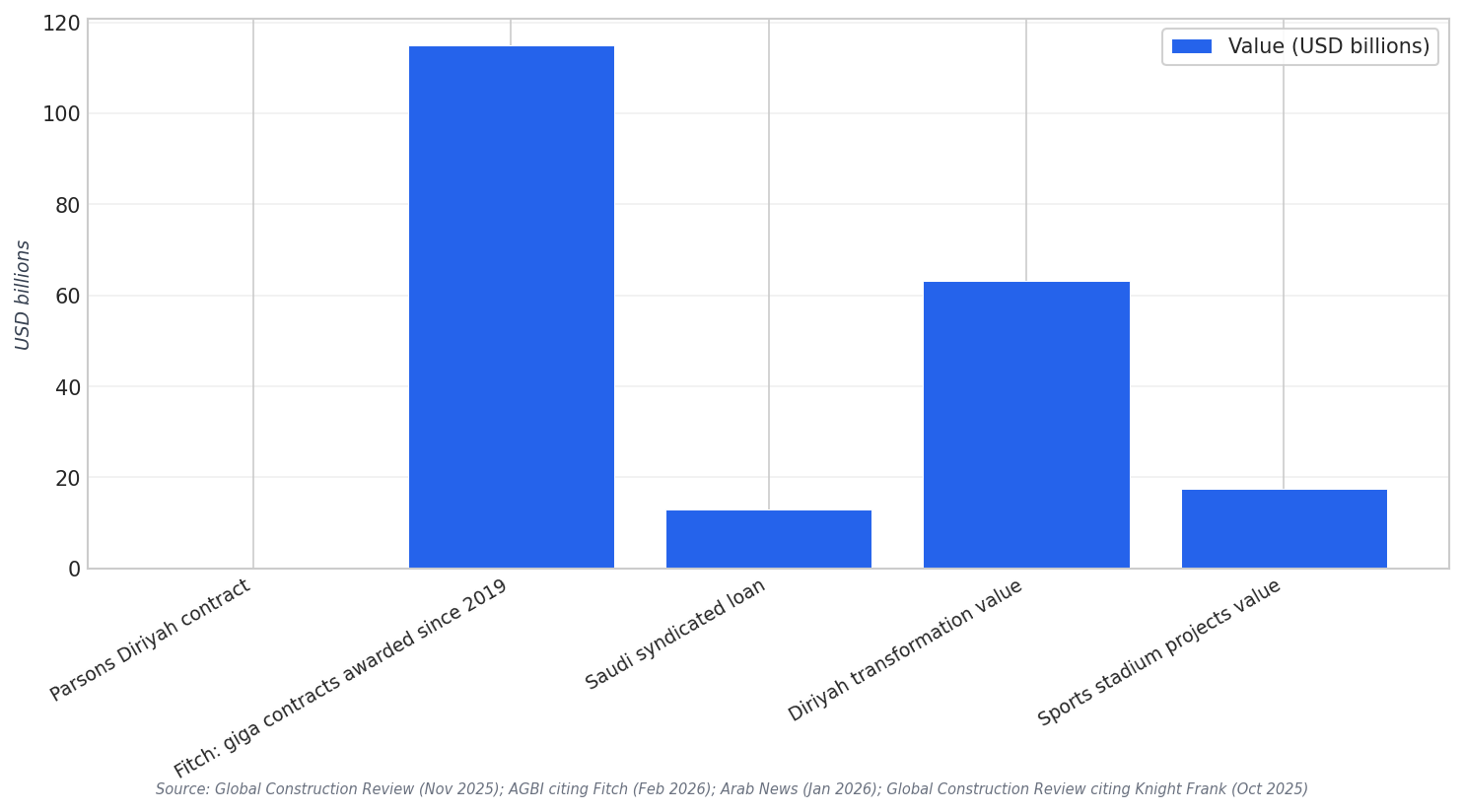

Funding and risk allocation are also evolving. Fitch Ratings estimates only $115 billion worth of giga-project contracts have been awarded since 2019, with roughly half of total funding, including debt and capital, coming from PIF, according to AGBI. In October, Al-Falih said giga-projects “have been taking a lot of resources from the government” and urged local and foreign investors to step in. Separately, Arab News reported Saudi Arabia raised $13 billion through a seven-year syndicated loan arranged by the National Debt Management Center to support infrastructure spanning power, water, and public utilities, aligning with Vision 2030 goals and private-sector participation.

Despite pullbacks in some areas, live procurement and award activity continues in others, and that matters for backlog quality. Global Construction Review reported Parsons won a $56 million five-year contract on Diriyah, covering parks, open spaces, and more than 55km of streetscapes, within a wider $63.2bn transformation; the first phase is designed to host 100,000 residents and attract up to 50 million annual visits. Knight Frank data cited by Global Construction Review also said annual contract awards in Saudi Arabia rose to $196bn, up 20% from 2024, and that sports infrastructure includes more than a dozen stadiums with a combined project value of $17.5bn. The reset, in practice, looks like selective prioritization, not an across-the-board freeze.

This chart compares contract and project values cited across sources, illustrating the scale of active work and the market’s pivot toward prioritized programs.

What is the Saudi Vision 2030 recalibration?

Which projects are being prioritized for near-term contracts?

What is happening with NEOM under the reset?

What do the sources say about funding pressure and the role of PIF?

Are contractors still winning major work during recalibration?