Across distribution networks, automation is no longer framed as a future bet. It is described as a present reality, with automated storage and retrieval systems, autonomous mobile robots, conveyors, and sortation technology operating alongside traditional labor on the same floor. But performance can still fall short even after the equipment is installed. One explanation offered in the sources is that the technology is not usually the constraint. The readiness of the people supporting it is. When labor is volatile and demand is uncertain, the tipping point arrives: a manual-first model becomes harder to stabilize and harder to scale.

Workforce pressure is a repeated theme. One industry view cites a shortage of skilled workers who combine manual skills with organizational skills, plus competition for warehouse personnel based on pay, benefits, and lifestyle. That same view frames automation as a way to augment the gap rather than replace people, with companies still planning to hire human workers. Another view emphasizes that jobs are shifting, with robots taking repetitive tasks while hiring is redirected toward technical roles. This is the operational math behind the warehouse automation GCC discussion: the labor challenge is not only headcount. It is capability, consistency, and fit for increasingly complex workflows.

The Real ROI Risk: Downtime and Readiness

Automation changes what “cost” means inside a warehouse. A source warns that unplanned automation downtime can routinely outpace the labor savings that justified the investment in the first place. It gives examples: a single conveyor failure during peak season, an AS/RS error that goes undiagnosed for hours, or a robot jam that halts outbound flow. Each can cost more than the headcount savings delivered that day. This reframes the tipping point for manual warehousing. It is not only that manual processes are expensive. It is that automated operations demand a workforce trained to operate, monitor, troubleshoot, and maintain systems so that the promised gains are not erased by stoppages.

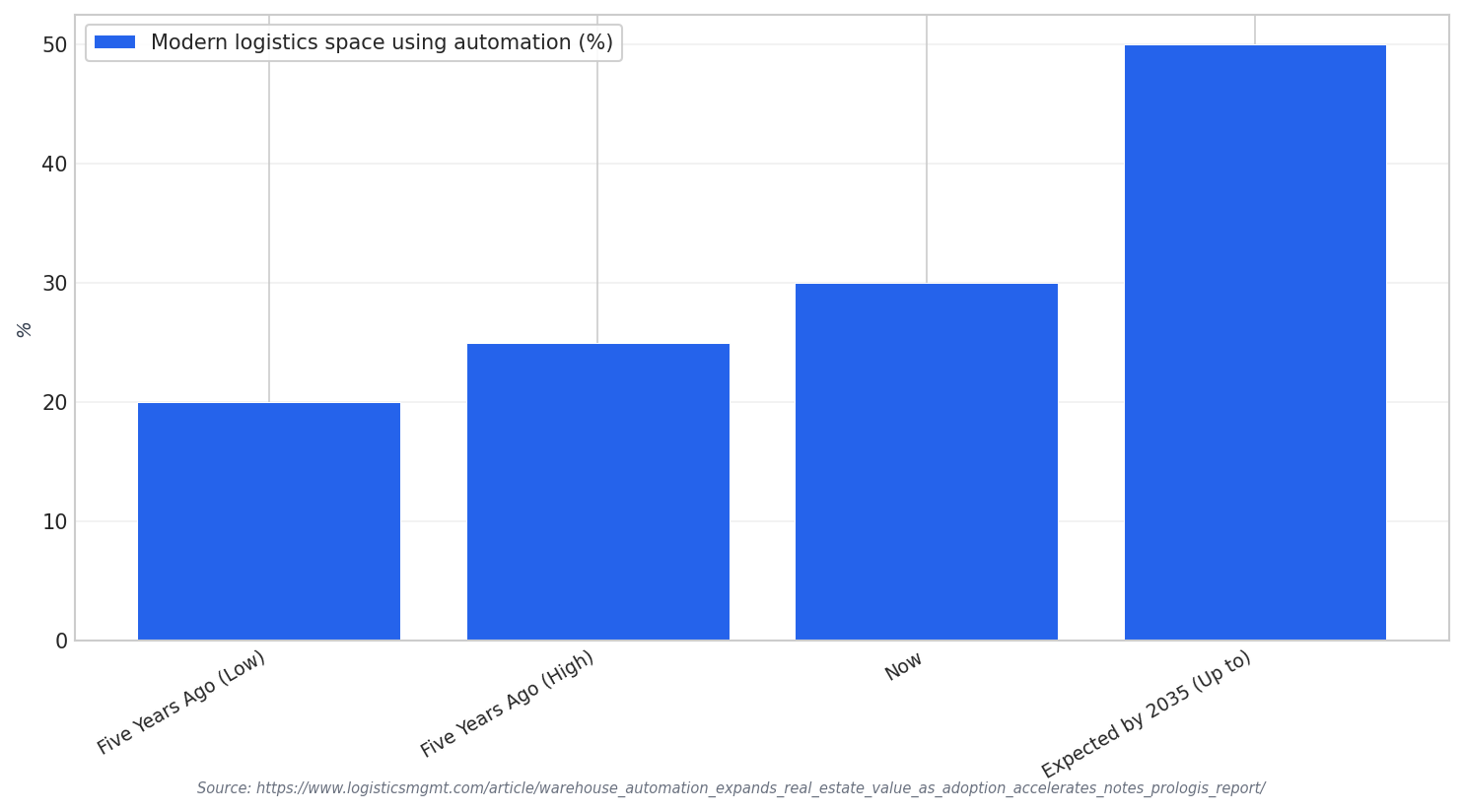

Spending intent and adoption signals support this shift. Interact Analysis findings cited in the sources say warehouse automation order intake for 2025 grew by 7% year-on-year, even after a period when many companies postponed large capital expenditure projects due to tariff uncertainty. A separate report notes that around 30% of modern logistics space now uses automation, up from 20% to 25% five years ago. It also states that automation is still early, with penetration expected to reach up to 50% by 2035, and that modular systems can offer faster ROI and be deployed in existing buildings. These are broader indicators, but they help explain why the manual-only model is losing its economic argument.

For the GCC context, the sources point specifically to the Middle East, particularly the UAE, investing heavily in smart logistics and warehouse automation. They link this to growth in trade and infrastructure development, and to demand for AI workforce assistants in the region. This does not provide GCC-wide adoption percentages, so it should be read as directional evidence rather than a full regional benchmark. Still, it supports a practical conclusion for warehouse automation GCC planning: automation investment and workforce design must be treated as one program. Winning operations are described as those where automation and workforce are integrated, prepared, and mutually reinforcing.

The tipping point becomes clear when you connect labor scarcity, shifting skill requirements, and the cost of downtime. If robots handle repetitive tasks while teams move toward technical roles, the warehouse must develop an “automation-ready workforce,” not a workforce “being replaced by machines.” Vendors and maintenance suppliers also appear in the operational picture. A 2026 outlook survey reports that 46% of companies ask providers to perform maintenance, 41% use them for consulting, 30% work with them on equipment upkeep and upgrades, and 28% for analysis. That mix suggests a shared responsibility model, but it also reinforces the same message: manual warehousing stops paying when complexity rises, and readiness becomes the main constraint.

It is also worth noting how quickly the market narrative is moving. One report states that one decade ago, automation was out of reach for many operations, while today it is described as more accessible, faster to deploy, and better. Another survey of warehouse decision-makers in Europe found that 82% agree increased use of technology and automation boosts frontline productivity, while 57% do not know where to start. For GCC operators, that “where to start” question is part of the tipping point. The most durable starting point in the sources is not a single machine. It is building the people, processes, and partner support needed to keep automation productive, safe, and continuously improving.

The following chart summarizes three time-based and forecast adoption figures reported for modern logistics space automation, providing a simple view of acceleration and the expected direction of travel. The values are: 20% to 25% five years ago, around 30% now, and penetration expected to reach up to 50% by 2035.

What is the “automation tipping point” in warehousing?

Does automation replace warehouse jobs?

Why can automation ROI fail even after installation?

What evidence supports accelerating automation adoption?

How does “warehouse automation GCC” relate to the UAE specifically?