Tariff volatility is no longer a background risk. It is shaping costs, supplier choices, and investment timing. For GCC leaders, the goal in 2026 is to avoid being a “victim of trade fragmentation” and instead build the capabilities to become a “leader in adaptive” management of disruption. The most practical starting point is to treat tariffs as a cross-functional issue. Pricing, procurement, finance, and operations must align on scenarios, trade-offs, and response triggers. This is the spine of a durable US tariffs GCC business strategy.

Begin with what can be stabilized fast. A three-phase roadmap used in the Gulf frames 2025–2026 as “emergency stabilization through price monitoring, diversification, and consumer protection.” In parallel, GCC businesses can map tariff exposure by product and supplier, because many firms lack visibility into the tariffs, duties, and freight they pay by product or shipment. That visibility is a prerequisite for better network decisions, including shifting purchasing terms to bring control over duties in-house and tracking import fees supplier-by-supplier.

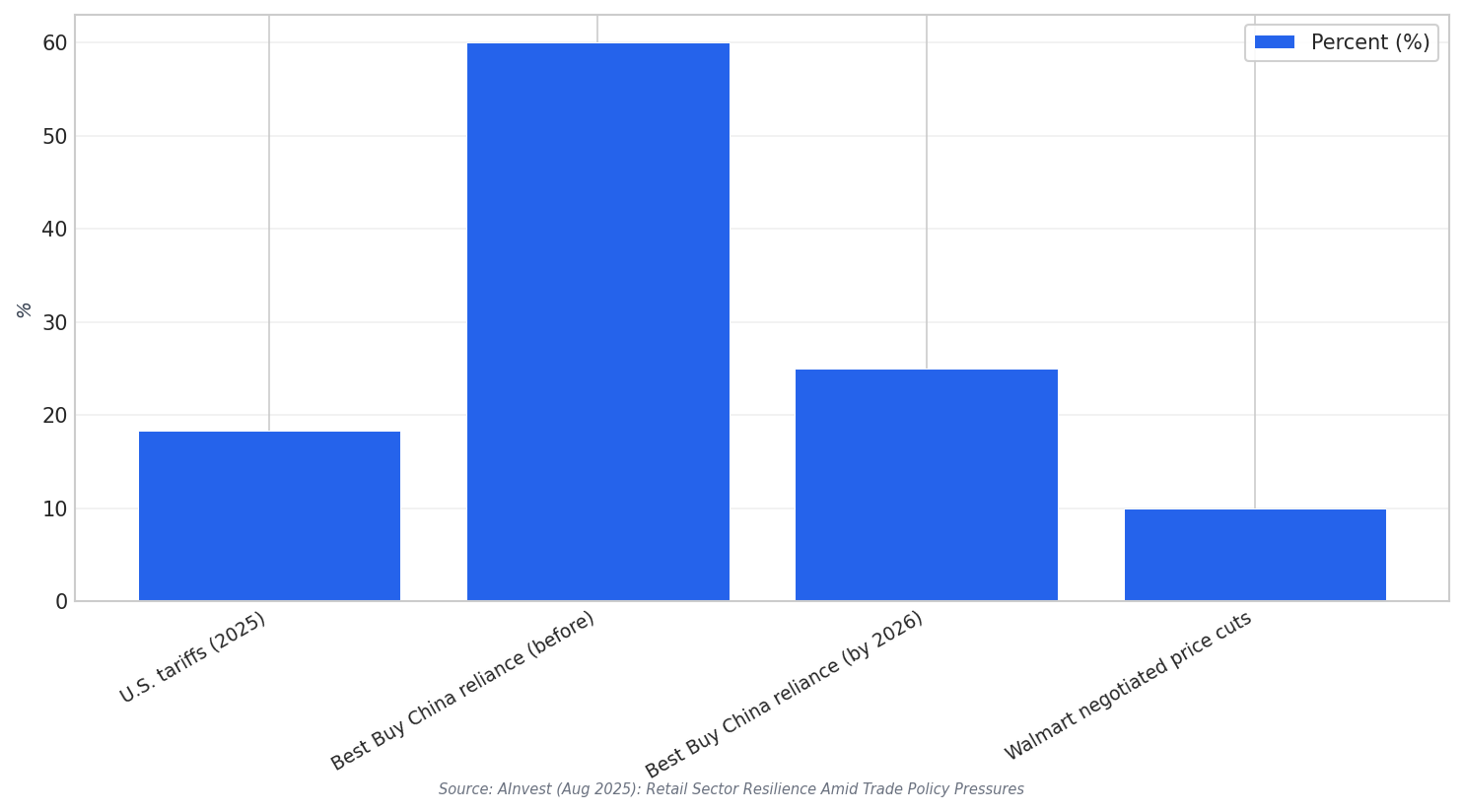

Global signals also show why diversification and pricing discipline matter. In the U.S. retail environment in 2025, tariffs reached 18.3%. That pressure drove “strategic pricing and margin management” and accelerated shifts away from concentrated sourcing. One example: Best Buy reduced reliance on China from 60% to under 25% by 2026 by sourcing more from South Korea and Vietnam. Walmart negotiated 10% price cuts from Chinese manufacturers while expanding partnerships in Southeast Asia. These examples are not GCC-specific, but they illustrate tactics that can inform 2026 playbooks in import-reliant categories.

A 2026 Operating Model: Cost Takeout, Data, and Regional Leverage

Tariffs tempt firms to freeze investment, but research on manufacturers warns against “mortgaging their futures” by avoiding long-term cost improvements. In a survey of 150 middle-market-to-large manufacturers, respondents used an average of four cost take-out tactics, showing that no single lever is enough. For GCC businesses, combine disciplined cost takeout with targeted investment in tools that improve decisions under uncertainty. Examples include demand forecasting, inventory optimization, and customs analytics, which can reduce errors in planning and limit overpayments in customs processes.

In 2026, pair company-level actions with GCC-wide coordination where possible. Gulf planning around food security highlights expanding strategic commodity reserves beyond bulk staples to include fresh and processed foods, which face the highest tariff pressures, supported by more climate-controlled storage. It also emphasizes regional coordination and integration: joint procurement programs across GCC states can create economies of scale and negotiating leverage, while regional food processing hubs and cross-border agricultural initiatives can add value to imports and create supply chain flexibility. This sets up Phase 2 (2026–2028) structural transformation through scaled domestic production and regional integration, and Phase 3 (2028–2030) optimization and global positioning.

What does a practical US tariffs GCC business strategy focus on in 2026?

Which diversification moves show what “good” can look like under tariff pressure?

How many cost takeout tactics do companies typically combine?

What regional actions can reduce GCC vulnerability to tariff disruption?