Vietnam is positioning itself as a connector in the next wave of supply-chain diversification. Vietnam’s Ministry of Industry and Trade described 2025 as defined by global uncertainty, where trade tensions, protectionist policies, geopolitical conflicts, and climate-related crises kept disruption risks high. In that context, enterprises in Vietnam have been pushed to diversify markets and increase supply-chain transparency. Industry voices also stress “localisation” and “multi-dimensional linkage” to reduce dependence on imported inputs and to raise domestic added value. This is not framed as optional. It is described as a survival tactic when major markets face shocks.

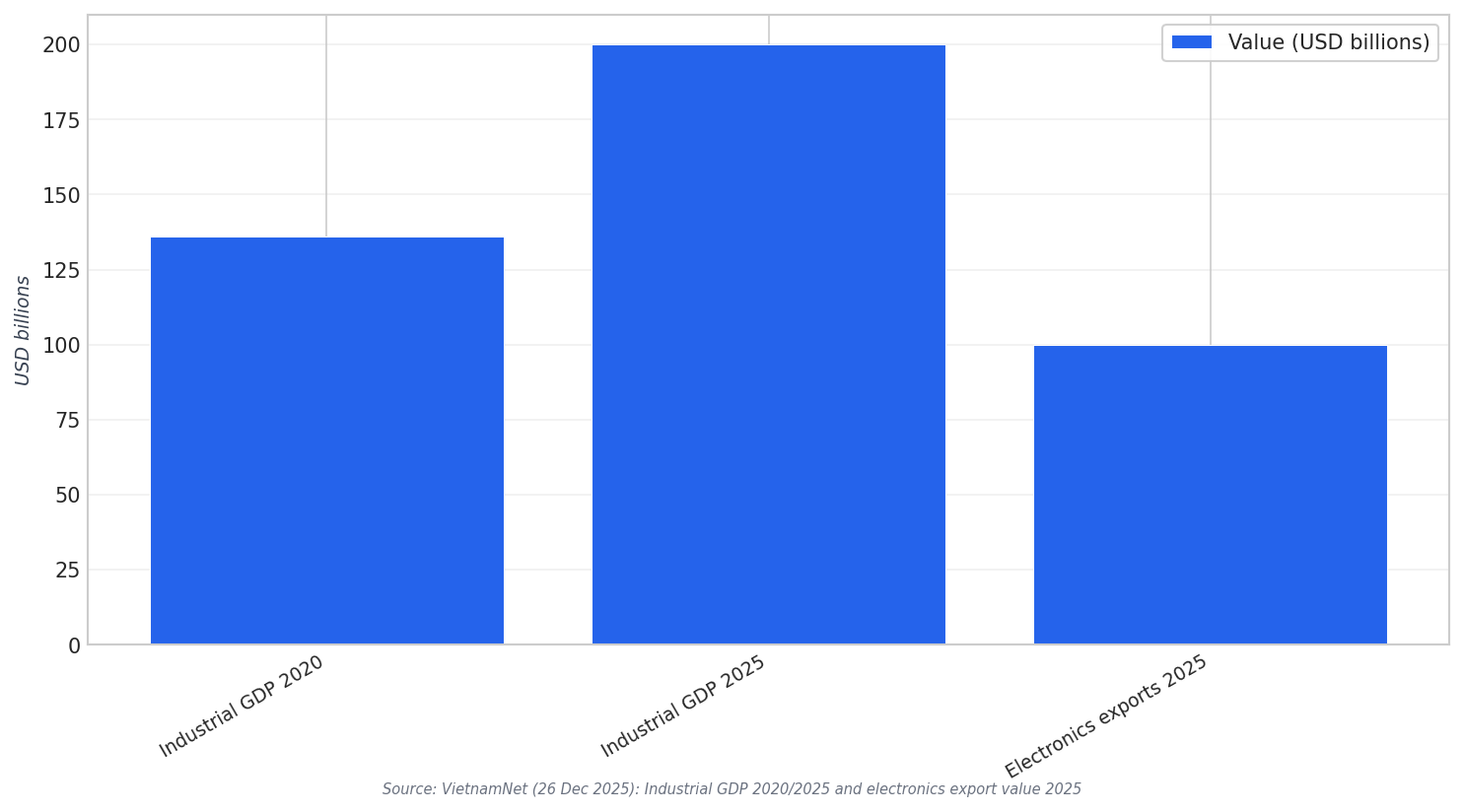

The numbers behind this connector role are visible in industrial performance. Vietnam’s industrial production grew 9.5% in 2025, the highest rate since the Covid-19 pandemic, alongside a shift from a traditional manufacturing base toward a more vital role in global supply chains. Industrial GDP reached about $200 billion in 2025, up from $136 billion in 2020. Electronics also became Vietnam’s largest export industry, valued at around $100 billion. VietnamNet also reported that electronics products make up 33% of total national exports, mainly produced by foreign-invested enterprises, highlighting both scale and dependence at the same time.

What Makes Vietnam a “Connector” in 2026

Logistics operators are describing how trade is physically reorganizing around Vietnam. DHL Global Forwarding Vietnam said global trade routes are stretching to record distances, with Vietnam emerging as a central hub, and that diversification and growing trade flows into and out of Vietnam are driving redesigns of air and ocean networks. DHL also described trade flows increasingly following a China–Vietnam–global pattern, and highlighted Vietnam’s role in processing and re-exporting goods. DHL Express said it recently invested in the north and in Hanoi “more than quadrupled” capacity, while noting the government is building a new airport to support future growth in the south. These statements point to a connector model built on routing flexibility and gateway capacity.

FDI is another pillar of the Vietnam connector economy in 2026, but it brings clear priorities for investors and suppliers. In Q1 2026, Vietnam’s GDP growth reached 7.83% and total registered FDI was estimated at around $15.2 billion, up 42.9% year-on-year. Disbursed capital reached $5.41 billion, the highest Q1 level in the past five years, with manufacturing and processing taking more than 70% of total capital. The same period showed expanding US commercial stakes: the US had over 1,500 projects nationwide with registered capital exceeding $12.5 billion, while Vietnam’s exports to the US reached more than $151.8 billion in 2025. These flows are increasing demand for logistics infrastructure and supply-chain development.

The profit opportunity in 2026 is not just about receiving diverted production. It is about upgrading what Vietnam can supply into those rerouted chains. UNIDO data cited by the Vietnam Association for Supporting Industries said Vietnam’s manufacturing value added reached 26.3% of GDP by 2023, approaching China’s 28.6%, yet experts still describe many local firms as stuck at basic processing and short of true OEM capability. The same forum noted a US business delegation explored relocating up to 30% of production volume to Vietnam if local suppliers could meet demand. In response, the Ministry of Industry and Trade called for a 2026 transformation toward higher productivity, quality, and value-added growth, aligning localisation, linkage, and execution with the connector role.

What is the Vietnam connector economy in 2026?

Which data points show Vietnam’s industrial momentum heading into 2026?

How is DHL responding to Vietnam’s expanding connector role?

What does Q1 2026 FDI suggest about supply-chain diversification into Vietnam?

Why do Vietnamese suppliers face pressure even as buyers look to diversify?