Indonesia’s geothermal story starts with a resource advantage tied to its volcanic geology. It is often reported that the country holds 40% of the world’s potential geothermal resources, estimated at 28,000 MW. Market research also cites national potential figures in the same order of magnitude, including around 28.5 GW of potential and another estimate of 23,965 MW concentrated across Java, Sumatra, Bali, and Sulawesi. That scale matters because geothermal delivers round-the-clock electricity, and it supports a baseload-oriented renewable strategy rather than only variable generation.

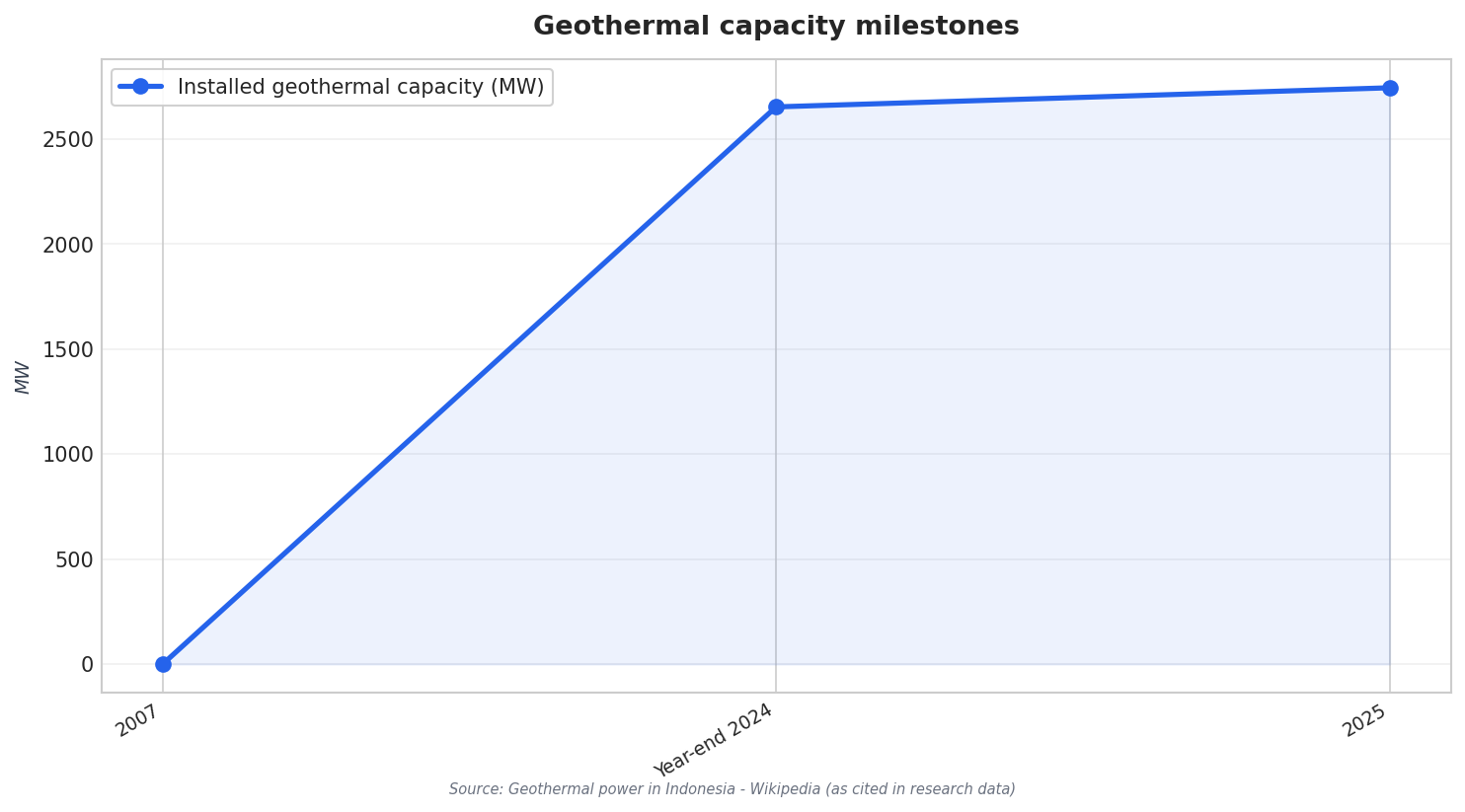

On deployment, Indonesia has moved into the top tier globally. Wikipedia reports 2,653 MW of installed geothermal capacity as of year-end 2024, and says Indonesia ranked second in the world after the United States (3,937 MW) and ahead of the Philippines. By 2025, Indonesia’s Ministry of Energy and Mineral Resources reported installed capacity had reached 2,744 MW (about 2.71 GW). Other sources describe lower “current installed capacity” snapshots, such as 2,276 MW, showing how totals can vary by reporting scope and timing. Still, the direction is consistent: capacity is rising and Indonesia is already a global heavyweight.

Targets, Roadmaps, and What “Becoming No. 1” Would Take

Plans and targets are now the main narrative driver of Indonesia’s geothermal buildout. Wikipedia notes that by 2025 Indonesia aims to produce more than 9,000 MW of geothermal power, framing a bid to become the world’s leading geothermal producer. Another market source states that Indonesia’s power development plan targets roughly 5.2 GW of geothermal capacity by 2034, alongside a specific goal to add 3.3 GW of new geothermal capacity by 2030. In the broader power system, Bloomberg’s sponsored piece cites a RUPTL roadmap calling for 42.6 GW of new renewable capacity by 2034, with more than 60% of new additions coming from renewables and geothermal positioned as a cornerstone.

Execution depends on converting resource potential into projects, and much of the opportunity remains undeveloped. A 2025 blog source puts Indonesia’s geothermal potential at 23.7 GW and says “over 21 GW is still untapped,” adding that resources are located in over 360 sites nationwide. Market concentration also shapes delivery: Nexdigm describes development clustered in Java and Sumatra due to high-temperature reservoirs and infrastructure that supports exploration and grid integration. It also values the Indonesia geothermal market at approximately USD 3.85 billion in 2024 and highlights government support through regulatory incentives, risk-sharing schemes, and financing mechanisms.

Developers are already adding capacity through upgrades and expansions, even as geothermal projects face long development cycles, high upfront investment, and complex geology. Bloomberg’s sponsored article says Barito Renewables, via Star Energy Geothermal, operates more than 900 MW, and expects capacity upgrades and new developments to add more than 100 MW in the next three years. Mordor Intelligence adds that Indonesia’s Pertamina Geothermal Energy added 165 MW across three Sumatra fields in 2025, and that Star Energy completed a 110 MW expansion at Salak to prolong reservoir life by 18 years. Put together, these moves illustrate how Indonesia can translate baseload reliability into momentum—if permitting, investment, and project delivery keep pace with the targets.

How large is Indonesia’s installed geothermal capacity right now?

What targets does Indonesia have for future geothermal capacity?

Where is geothermal development most concentrated in Indonesia?

Which companies are driving new projects and expansions?

What is the outlook for Indonesia’s geothermal energy expansion?