Thailand is being positioned as South-east Asia’s largest car manufacturing hub, and Chinese EV makers are treating it as a launchpad. A generous mix of subsidies and tax breaks has made Thailand an early destination for Chinese EV companies. BYD, Great Wall Motor, SAIC, Changan, Chery, and GAC are among the carmakers that have already set up plants there. The manufacturing push is part of a wider wave of factories across South-east Asia that begin producing Chinese EVs in 2026, driven by a saturated market in China and incentives from host countries. This momentum is central to the “Thailand EV manufacturing hub” narrative now taking shape.

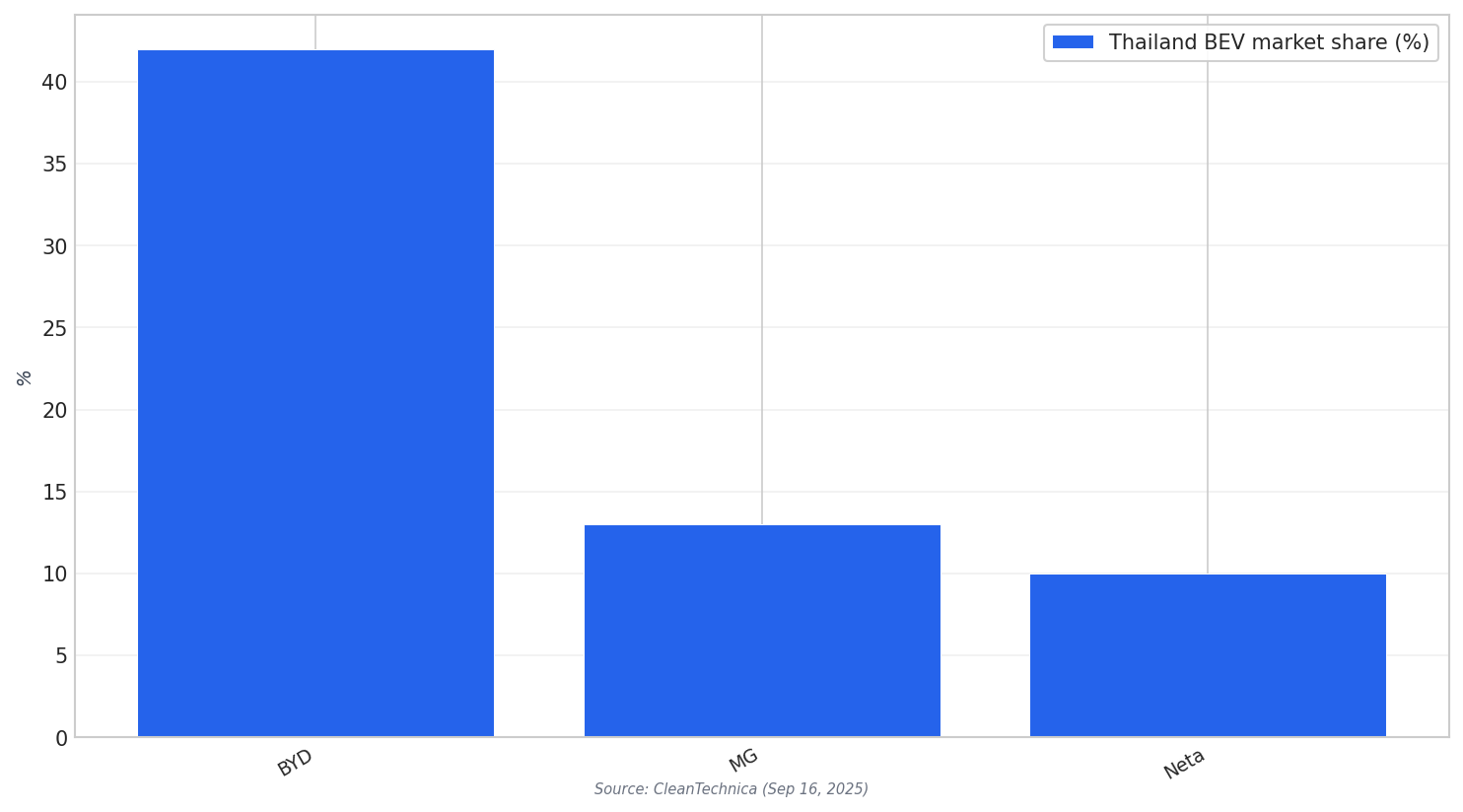

Thailand’s EV market has also become a battleground for share. Chinese brands dominate the EV market in Thailand with a combined share of more than 70%, according to Reuters. CleanTechnica reports Chinese automotive manufacturers collectively achieved 65% market share in Thailand’s BEV sector, with BYD at 42%, MG at 13%, and Neta at 10%. Reuters also cited that BYD had a 49% share in 2023, while Counterpoint data showed Neta peaked at around 12% of EV sales in 2023. The surge in brands is pressuring smaller players, with the number of Chinese EV brands in Thailand doubling in the last year to 18.

From Price Wars to Production Quotas: The New Rules of the Hub

Competition is not only happening in showrooms. Reuters described pricing as “the main strategy to stimulate buying,” as China’s EV overcapacity and price war spill into Thailand. That stress is visible in Neta’s downturn: in the first five months of the year referenced by Reuters, new registration of Neta cars slumped 48.5% from the prior year, and its share of EV registrations fell to 4%, based on government data. Meanwhile, policy targets remain bold. Reuters reported Thailand unveiled a plan three years earlier to ensure at least 30% of its total auto production was EVs by 2030, while also noting the country exports about half of its auto output.

Thailand is also adjusting incentives to keep factories moving even when local demand is weak. Automotive World reported that Thailand revised its EV incentive policy to give automakers more flexibility in meeting production requirements. For the first time, exported vehicles can count toward local manufacturing targets, and one exported EV counts as 1.5 vehicles toward production quotas. This matters because Thailand is being built as a regional production and export hub, not only a domestic sales market. CleanTechnica described BYD’s Thailand facility as a Southeast Asian production base that can potentially supply neighboring markets, including Malaysia, Indonesia, and Vietnam.

Chinese OEM investment plans show how localization is being executed. Reuters reported Thailand has drawn more than $3 billion in investments from a clutch of Chinese EV makers, including Neta, linked in part to the government incentive scheme. CleanTechnica detailed capacity targets and commitments: Changan targets 100,000-unit annual capacity by 2025, while Chery projects 50,000-unit production in 2025 and expansion to 80,000 units by 2028. AION committed THB 2.3 billion ($72.6 million) for a 20,000-unit annual production capacity. Still, analysts cited in regional reporting questioned how much local workers will benefit, pointing to limited technology transfer and reliance on Chinese suppliers in some cases.

Why is Thailand becoming a Thailand EV manufacturing hub for Chinese OEMs?

How dominant are Chinese brands in Thailand’s EV market?

What market share did BYD, MG, and Neta hold in Thailand’s BEV sector?

What happened to Neta’s performance in Thailand according to Reuters?

How did Thailand change EV incentive rules related to exports?