The Qatar LNG North Field expansion is increasingly driving price expectations through timing and negotiating leverage, not just nameplate capacity. QatarEnergy’s CEO signaled that output would begin in the second half of 2026, turning that year into a point when “first new Qatari volumes begin influencing negotiation leverage, portfolio planning, and the psychology of procurement committees across Asia.” The key is that these volumes arrive while contracting decisions for the late 2020s and early 2030s are actively being negotiated. That overlap makes 2026 a live pricing moment, rather than an end-state for the market.

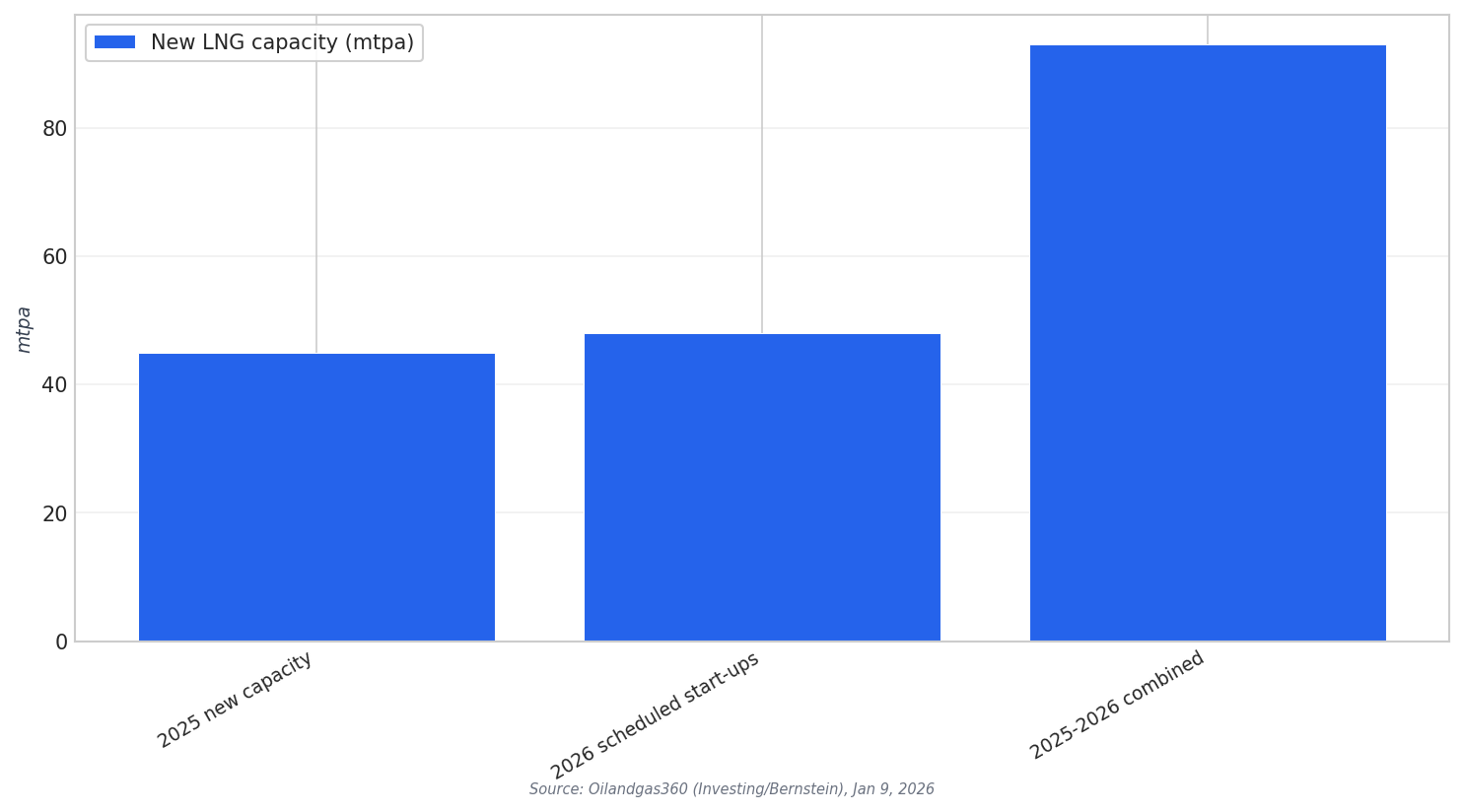

On paper, the supply wave is large across the industry, and it frames how buyers model LNG affordability. Bernstein highlighted that around 45 mtpa of new LNG capacity began ramping up in 2025, with another 48 mtpa scheduled to start up in 2026. That is roughly 93 mtpa across 2025 and 2026. Bernstein also estimated that about 150 mtpa of incremental LNG supply will hit the market between 2026 and 2028, describing it as roughly 35% of current global demand in just three years. In that context, Qatar’s added volumes can push negotiations toward a buyers-market mindset.

Security Shocks Can Reprice the Same Supply Story Overnight

Geopolitics can invert the narrative from surplus to scarcity, and the Ras Laffan attacks show why contract pricing builds in disruption risk. Qatar produced an average of 6.7 MMt of LNG per month in 2025, and analysis cited that a five- to six-month disruption would push global supply into year-on-year decline. Each additional month of downtime could remove roughly 1.5% of annual LNG availability. Qatar also declared force majeure in early March, removing approximately 80 MMtpa of LNG supply—nearly 20% of global availability—from the market. Those numbers explain why buyers can reprice security premiums even while expecting large future capacity additions.

The timeline for the North Field expansion itself became part of market pricing when disruptions raised delay risk. Wood Mackenzie analysis warned that the disruption threatens to delay Qatar’s North Field East expansion, which was expected to add 32 MMtpa of capacity, and that any slippage into 2027 or beyond could constrain global LNG supply growth through 2028. Bloomberg reported that QatarEnergy was pushing back the start of a major expansion project to at least 2027 after a drone attack that forced the unprecedented closure of Ras Laffan, with North Field East targeting its first export early next year if the outage extends for a month or less. For Asian buyers—who account for roughly 90% of Qatar’s LNG exports—small schedule changes can quickly feed through into long-term pricing assumptions.

By 2027, the volume headline becomes hard to ignore. Reuters reported that at full production, the North Field expansion project is expected to produce 126 million metric tons of LNG per annum by 2027, boosting QatarEnergy’s output by some 85% from its current 77 mtpa. In parallel, Reuters also cited a projection that LNG demand could reach 600–700 million tonnes per annum by 2035, with rising energy needs from artificial intelligence named as a driver. Put together, these facts clarify how Doha can “reprice” the market: it strengthens its hand in contract architecture by offering scale, while buyers re-evaluate risk premiums under both supply-wave and disruption scenarios.

What is the Qatar LNG North Field expansion expected to produce by 2027?

When is first output from the North Field expansion expected to start?

How big is the broader LNG supply wave around 2025 and 2026?

How can Ras Laffan disruptions affect LNG availability and pricing?

Why does 2026 matter for long-term LNG contracts in Asia?