The UAE’s move toward a single, more consistent approach to health coverage is reshaping how benefits are defined, delivered, and financed. A key pillar is the directive to adopt a unified national health insurance system for Emirati citizens across all seven emirates, aimed at ensuring comparable access and service standards regardless of where a citizen lives or receives treatment. This change is framed as a transition from varied emirate-level programmes to a federal umbrella that reduces disparities in coverage scope, access mechanisms, and service quality. At the same time, nationwide enforcement of compulsory coverage is expanding the insured population and intensifying the operational demands placed on insurers, employers, and administrators.

For residents and employers, the rollout of mandatory coverage from January 1, 2025 is a major structural driver. The basic scheme described by the Ministry of Human Resources and Emiratisation sets a package priced at AED 320 (USD 87.11) per year and states there is no waiting period for chronic diseases. In parallel, market reporting points to rapid expansion in insured activity: Central Bank 2024 statistics cited by Gulf Business indicate health insurance premiums rose 20.9% year-on-year to Dhs31.3bn, while the number of policies increased 59.9% to 2.2m. Mordor Intelligence also notes the January 2025 mandate obligating private-sector employers to provide health insurance added roughly 2.5 million expatriates to the insured pool, while a separate Mordor report on the broader MENA market cites an estimate of about 3.7 million new lives added under the January 2025 requirement for every resident to carry a health policy.

What Changes for Insurers, TPAs, and Distribution

For insurers and third-party administrators (TPAs), a more unified operating environment can still mean higher complexity, not less. As the insured pool grows, utilisation and claims management become central, and Gulf Business highlights the need for effective regulation, co-payment frameworks, and proactive management of claims utilisation to avoid destabilising the market. In the UAE health insurance TPA segment, Mordor Intelligence reports that claims processing accounted for 45.7% of market share in 2024, while insurance companies represented 70.1% of end-user share in 2024. The same report notes that Dubai held 55.2% revenue share in 2024 and that administrators are investing in UAE-based cloud infrastructure and sovereign-hosting partnerships to comply with 25-year on-shore retention requirements, reinforcing that compliance and data handling are becoming a cost and capability differentiator.

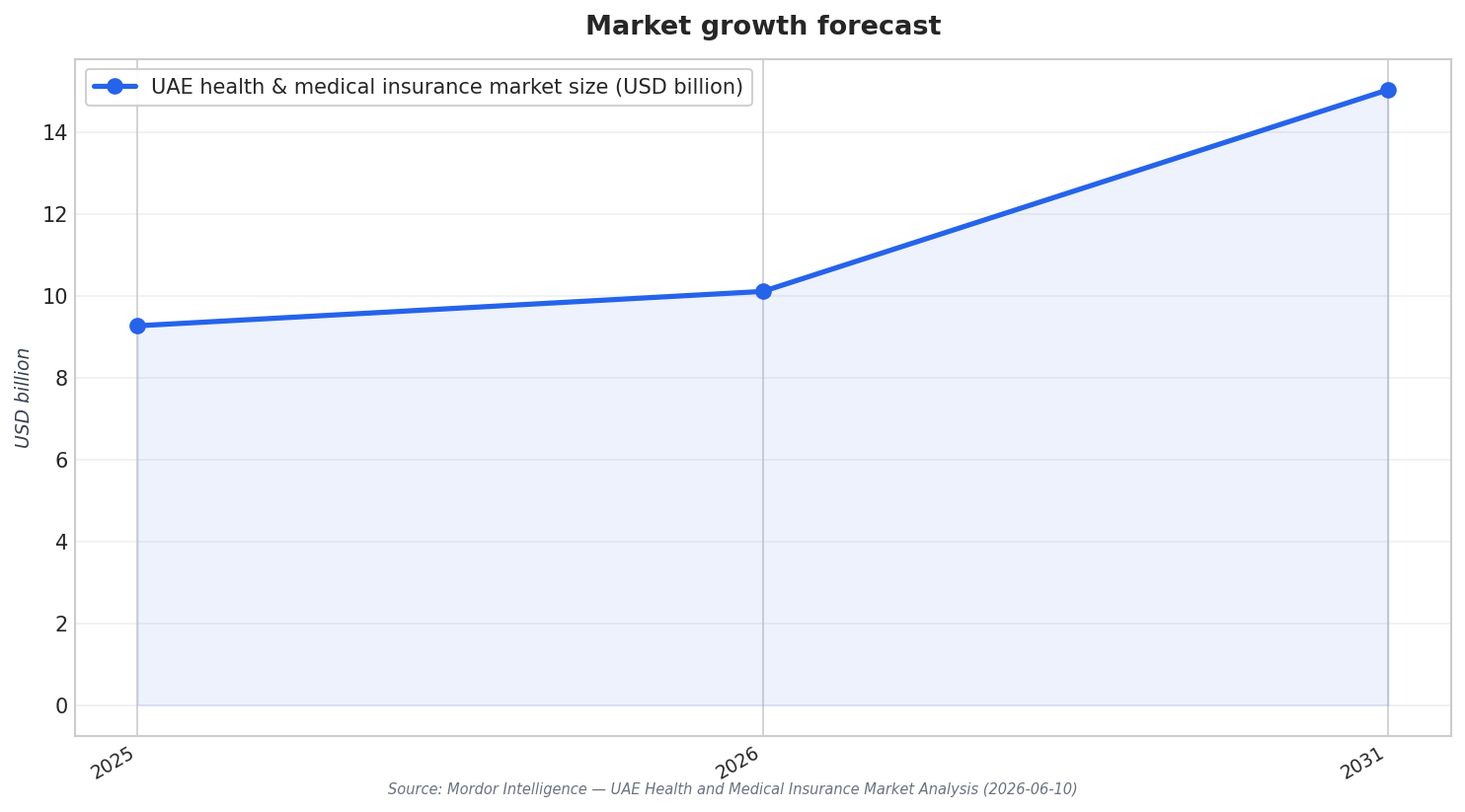

The commercial opportunity remains significant, but it will likely reward scale and strong distribution. Mordor Intelligence estimates the UAE health and medical insurance market is expected to grow from USD 9.27 billion in 2025 to USD 10.11 billion in 2026, reaching USD 15.04 billion by 2031 at an 8.26% CAGR over 2026–2031. The same source shows group policies led with a 72.69% share in 2025, while private insurers held 92.64% share in 2025. Brokers and agents accounted for 66.89% share in 2025, but online platforms are projected to grow fastest at a 13.87% CAGR through 2031. Mandatory policies also dominated with an 86.22% share in 2025, while Dubai represented 58.75% share of the market in 2025, and the Northern Emirates are forecast to expand at a 9.96% CAGR through 2031.

For citizens, the UAE unified health insurance framework is positioned as a practical promise of portability and consistent standards across the federation. Gulf News points to the current landscape of different citizen programmes, such as Thiqa in Abu Dhabi and Saada and Enaya in Dubai, alongside more varied coverage levels across Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah, and Fujairah. iPMI Global describes the change as removing geographical and administrative barriers that previously restricted coverage outside emirate-specific boundaries, citing local experience that families faced burdens when treatment costs were not fully covered outside their home emirate. For the ecosystem, the policy direction also aligns with more digital coordination, with Mordor Intelligence citing Abu Dhabi’s Malaffi health information exchange connecting all hospitals and a large network of clinics and clinicians, enabling stronger adjudication and utilisation management.

What is the UAE’s unified national health insurance system trying to achieve for citizens?

How did premiums and policy counts change, according to Central Bank 2024 statistics cited in Gulf Business?

What is the AED 320 basic scheme mentioned in connection with the 2025 mandate?

What does Mordor Intelligence report about the role of group policies and distribution in the UAE market?

How does the UAE unified health insurance framework affect insurers and TPAs operationally?