Indonesia’s strategy to turn nickel into leverage over the global EV transition is being tested by a fast-moving battery pivot in China. Asia Times reported that BYD’s new Datang SUV recorded 150,000 pre-orders in 53 days in China, and those orders were booked without “a single gram of nickel” in the vehicle’s battery. For years, one market assumption held that long-range EVs needed high-nickel ternary batteries to ease range anxiety. The Datang’s reception suggests that assumption is weakening in the world’s most important EV supply ecosystem, with direct implications for how Indonesia positions itself across the Indonesia nickel EV battery supply chain.

The shift is not only about chemistry. It is also about product economics and consumer acceptance at the premium end. Asia Times contrasts BYD’s older scale model, the now-discontinued F3 that retailed around 50,000 yuan (about US$6,900), with the Datang’s 239,900 to 309,900 yuan price band (roughly US$36,000 to US$46,500). BYD says the Datang runs on its second-generation Blade Battery; analysts believe, based on patent filings and a 3.8-volt platform, that it uses Lithium Manganese Iron Phosphate (LMFP), though BYD has not officially confirmed the cathode material and a prior filing described standard LFP. Either way, the formulation drops nickel and cobalt in favor of lithium, iron, phosphorus, and manganese.

Why This Battery Pivot Hits Indonesia’s Nickel Playbook

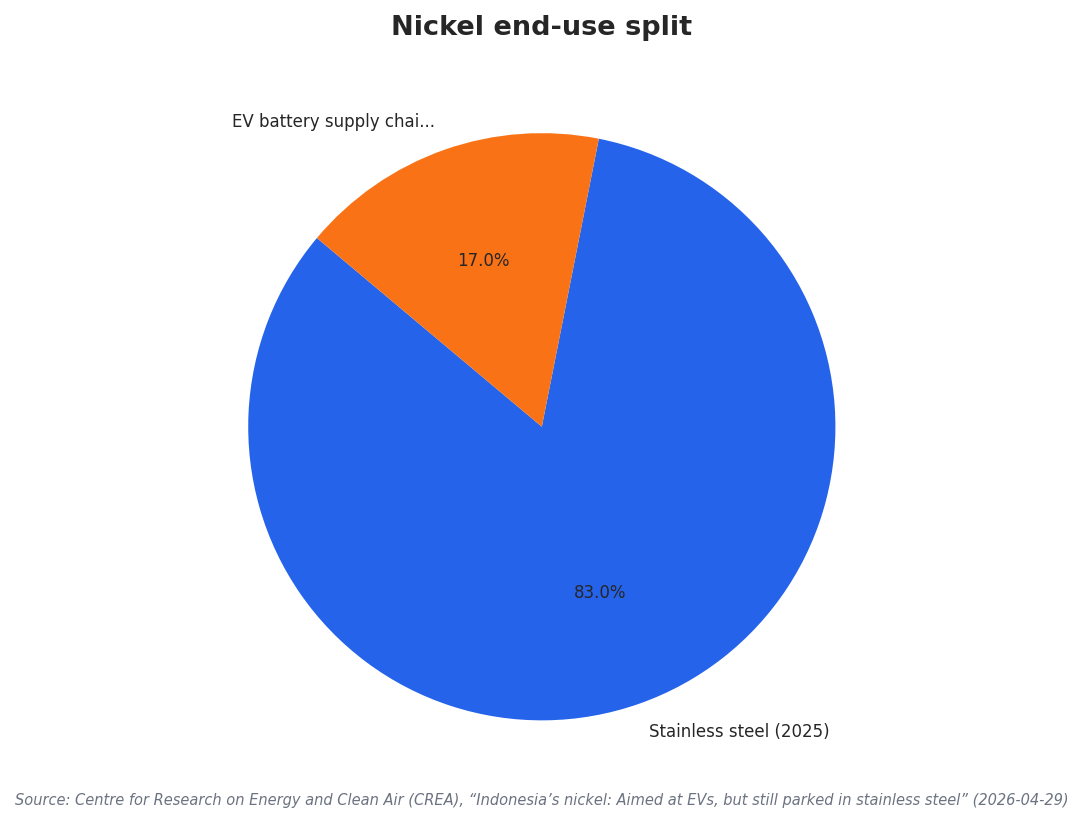

Indonesia’s nickel story is often branded as EV-driven, but the current end-use split shows a more complicated picture. A Centre for Research on Energy and Clean Air (CREA) report found that 83% of Indonesia’s 2025 nickel production was absorbed by the stainless steel sector, while only 17% went into the EV battery supply chain. At the same time, CREA notes that nickel-free batteries are gaining traction globally and that LFP batteries command over 80% of the Chinese market, citing lower costs and longer lifespans. If the biggest battery market is already dominated by chemistries that do not require nickel, then Indonesia’s downstreaming push faces a demand-side risk, not just a production challenge.

Indonesian policy has aimed to pull more value onshore by pushing processing and attracting foreign investment. A CSIS analysis notes that the nickel export ban persuaded foreign companies to set up processing plants in Indonesia, and that nickel processing for use in batteries started in 2021, with more projects in the pipeline mainly due to Chinese investments. CSIS also says South Korean investments are building the country’s first EV battery plant scheduled to start production in 2024, along with its first EV plant. Whether Indonesia can reach its goal to produce 140 GWh in 2030, CSIS argues, depends on attracting substantial foreign investment over the next few years—investment assumptions that look different if nickel demand in batteries keeps being engineered down.

The political framing has been explicit. A 2025 report by the Center for Research on International (CRI) notes that Indonesia’s investment minister announced in January 2023 that the country was considering forming an “OPEC-style cartel” for nickel and other battery raw materials. But cartels require captive buyers. Asia Times argues that Indonesia’s attempt to dominate high-margin battery supply chains depends on a technical dependency that the market is actively engineering around. Indonesia is also trying to expand beyond saprolite into limonite-linked battery inputs, according to The Jakarta Post, which says a limonite-based production chain has begun to take shape. Yet if nickel-free batteries keep improving, Indonesia may need to rethink what “battery leadership” means—and how to compete when chemistry choice shifts faster than industrial policy timelines.

What is the nickel-free battery development that is pressuring Indonesia’s nickel strategy?

How much of Indonesia’s nickel is actually going into EV batteries today?

How dominant are nickel-free battery chemistries in China, according to the sources?

What investment milestones does CSIS cite for Indonesia’s battery industrial plan?

What does the Indonesia nickel EV battery supply chain risk if nickel-free batteries keep gaining ground?